#37 - WK24

The Quiet Toll

Numbers rarely tell the whole story. but sometimes they come close. This week, India posted a full-year GDP growth figure of 7.7%, with the final quarter alone clocking 7.8%. That is not a rounding error or a statistical quirk. India’s stronger-than-expected GDP print was one of the most talked-about data points in economic circles this week, arriving at a moment when much of the world is bracing for slower growth, disrupted supply chains, and the lingering shadow of an unresolved West Asia conflict pushing energy costs upward.

And yet, the very institution that should be celebrating, the Reserve Bank of India chose caution over applause. RBI Governor Sanjay Malhotra kept the repo rate unchanged at 5.25% and retained a neutral monetary policy stance, citing rising risks from the prolonged West Asia conflict, elevated energy prices, supply-chain disruptions, and weather-related uncertainties. What that essentially means: borrowing costs stay where they are. The RBI is watching, waiting, and not quite ready to declare the good times fully here. It also revised the GDP growth forecast for the current fiscal year downward to 6.6% from 6.9%, while raising its inflation projection to 5.1%. The message from Mint Street was careful and deliberate, we are growing, but the road ahead has potholes we can’t yet see clearly.

For anyone tracking jobs, markets, or the cost of everyday goods, that combination, strong past performance, cautious future outlook is worth paying attention to. It means Indian companies will be making conservative plans, consumers may not see loan rates fall anytime soon, and the rupee’s recent weakness continues to ripple through import costs.

Across the world in Europe, a different kind of inflection point was quietly ticking toward its deadline. The European Union’s most comprehensive reform of its Common European Asylum System (CEAS), comprising eleven legislative acts was due for implementation across all member states by June 12, 2026, with the same rules on asylum procedures set to apply uniformly across the bloc for the first time. The idea, years in the making, was to replace a patchwork of national systems with something coherent: faster decisions, border screenings, a solidarity mechanism between countries, and mandatory identity checks. The reform essentially aims to improve control at the external borders, with swift border procedures for people with poor prospects of remaining in Germany and clearly defined responsibilities replacing the dysfunctional Dublin System.

Whether it works as intended is a separate question. Several EU member states had not yet fully incorporated the new requirements into their national legal frameworks by the rollout date, with numerous outstanding IT issues still needing months of work to resolve. What is certain is that this reshapes how Europe manages migration and migration policy, whether one agrees with the direction or not, shapes labour markets, housing pressure, and the daily texture of life in German cities and beyond.

Speaking of rules that arrived late: also this week, the EU Pay Transparency Directive, which required employers across Europe to disclose salary ranges and close the gender pay gap hit its transposition deadline of June 7, and Germany missed it. The old rules remain in place for now. Under the new directive, job applicants would have been entitled to salary information before interviews, and employees would have gained the right to compare their pay against colleagues, broken down by gender changes that Germany’s own data suggests are long overdue, given that the country’s unadjusted gender pay gap sat at 18% in 2024, one of the highest in Europe.

Three stories, three different timelines, India building momentum while staying alert, Europe rewriting the rules on who gets in, and Germany still sorting out whether it believes in equal pay on paper and in practice. That is Week 24. Let’s get into it.

Stock Market

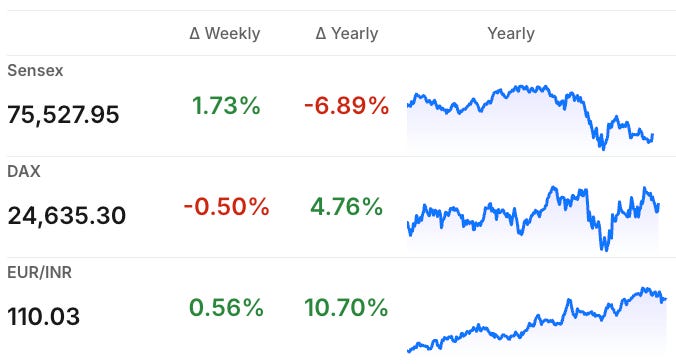

India's GDP expanded 7.8% in Q4 FY26, lifting full-year growth to 7.7% and markets spent most of the week digesting what that means alongside the RBI's cautious response. The Reserve Bank of India kept its repo rate unchanged at 5.25% and revised its growth forecast for the current fiscal year down to 6.6%, while raising its inflation projection to 5.1%, citing risks from the prolonged West Asia conflict, elevated energy prices, and supply-chain disruptions. The real push came on Friday, when a global rally fuelled by optimism around a looming US-Iran deal lifted the Sensex 2.29%, with broad-based gains led by banking, financial, realty, auto, and consumer stocks. Bajaj Finance surged 5.6%, Larsen & Toubro gained 4.9%, and Tata Motors added 4.1%, while the IT sector lagged with Tech Mahindra slipping 2.2%.

Germany's DAX had a turbulent week before clawing back ground on the final day. On Wednesday, June 10, the DAX fell 0.97% to close near 24,195, its lowest since mid-May driven by renewed global technology sector weakness, energy-sector disappointments, and broader pressure from elevated Middle East tensions and rising US inflation. Commerzbank fell over 2%, reflecting concerns about credit quality in Germany's corporate loan book amid a contracting economy and high energy costs. Friday brought relief: the DAX jumped nearly 2% as President Trump cancelled planned strikes on Iran and indicated a peace deal could be imminent, pushing oil prices lower. Deutsche Bank led gains at 6.6%, followed by HeidelbergCement and Siemens Energy.

Germany News Roundup

Fuel Price Cap: Germany implemented the new "Noon Price Rule" alongside the end of tax cuts to stabilize volatile fuel market rates.

Balkan Investment Push: Germany and France launched a joint Western Balkans initiative at the Montenegro EU summit to fast-track economic integration.

Aviation Safety: DLR developed "Hawkeye," a data-driven cockpit application designed to help pilots instantly select alternate airports during emergencies.

Energy Transformation: Germany introduced historic local energy-sharing regulations allowing citizens to sell surplus solar power directly to neighbors.

Drone Integration: Germany launched the "Swarming" project to research how multiple uncrewed ground and aerial vehicles can be controlled from a single command center.

Transit Strategy: Deutsche Bahn launched a competitive €99.99 Family Ticket to boost national rail transit and travel business revenues

India News Roundup

PM Milestone: The Union Cabinet passed a 7-point resolution congratulating Narendra Modi on completing 4,399 continuous days as India's longest-serving elected PM

Defence Tech: The Ministry of Defence signed a ₹449 crore contract with Accord Software to procure indigenous ECGNSS Jammers for the Indian Navy.

IPO Surge: Reliance Jio and the National Stock Exchange (NSE) are preparing for blockbuster IPO filings to revive the primary fundraising market.

SME Listings: Leapfrog Engineering and Clay Craft scheduled their respective ₹88.51 Cr and ₹110.11 Cr SME IPO launches for mid-June.

Textile Expansion: The Ministry of Textiles targets doubling India’s domestic textile market to ₹33 lakh crore by FY31, creating nearly 2 crore new jobs.

Corporate Lifeline: Aditya Birla Group announced an infusion of ₹4,730 crore into debt-ridden Vodafone Idea via convertible warrants for network expansion.

Opportunity

FCNR(B) Deposit

Something unusual happened in Indian banking this week, and it flew under the radar for most people outside the financial world. On June 8, the Reserve Bank of India quietly opened a three-month window running until September 30, 2026, that could allow overseas Indians to earn returns on dollar deposits that have no parallel in conventional fixed income anywhere in the world right now.

The instrument at the centre of it is called an FCNR(B) deposit shorthand for Foreign Currency Non-Resident (Bank) deposit. In plain terms, it is a fixed deposit held in Indian banks, denominated in foreign currency dollars, euros, pounds so the money goes in and comes back out in the same currency, without any rupee exchange risk to the depositor.

What the RBI did this week

The trigger for this week’s excitement was the RBI’s decision to absorb the entire cost of hedging currency risk on behalf of banks estimated at around 3 to 3.5% for all fresh FCNR(B) deposits mobilised between June 8 and September 30, 2026. This is the key move. Normally, when an Indian bank takes in dollar deposits and deploys them in a rupee economy, it has to pay a significant cost to insure itself against currency movements. By picking up that cost entirely, the RBI effectively allowed banks to pass much higher returns to depositors.

The banks responded almost immediately. The RBI circular allows banks to mobilise fresh FCNR(B) deposits with tenures ranging from three to five years. Deposits under the scheme carry a one-year lock-in period. AU Small Finance Bank is offering up to 7.1% on five-year US dollar deposits, among the highest rates in the market. YES Bank has revised its peak USD FCNR(B) deposit rate to 6.6% for five-year deposits. ICICI Bank and Axis Bank raised interest rates on FCNR(B) deposits to as high as 6% for deposits with maturities of three to five years, matching the peak rate with SBI and HDFC Bank.

To put that in context: five-year US Treasury notes currently yield around 4.3%, meaning some Indian banks are offering a premium of nearly three percentage points to attract NRI funds. This is a bank deposit, guaranteed principal, foreign currency denomination, no stock market volatility paying meaningfully more than US government bonds.

The leverage angle: where returns become extraordinary

The story does not stop at headline deposit rates. The RBI has also signalled openness to banks providing standby letters of credit to lenders who finance deposit customers. This means depositors can potentially borrow against their own FCNR(B) deposits abroad at lower rates, and use that borrowed capital to place even more into the high-yielding deposits amplifying returns significantly.

Why is the RBI doing this?

This is not charity. India’s rupee has been under pressure from elevated crude oil prices and global supply-chain disruptions. The RBI wants to bring in fresh dollar inflows to bolster foreign exchange reserves and ease pressure on the currency. The playbook is borrowed from 2013, when a similar scheme attracted over $34 billion and helped stabilise the rupee during a global emerging-market sellout.

What to keep in mind

The scheme is available only until September 30, 2026, a genuine three-month window. Deposits must be held for at least one year. The returns are in dollars, which removes rupee depreciation risk for the principal, but taxes in your country of residence still apply and must be factored in. Smaller banks are offering higher rates precisely because they have more ground to cover in building an NRI deposit base, which means slightly more counterparty consideration compared to large public-sector lenders.

This opportunity is uncommon enough that it is worth speaking to a financial advisor familiar with NRI investment structures before acting. But the underlying setup, an RBI-backed window, a short eligibility period, and dollar returns materially above US Treasuries, is the kind of thing that rarely surfaces in fixed income.

Until Next Sunday…

Conclusion

Navigating the fast-moving business world requires a fine balance between tracking big headlines and recognizing the quieter, everyday shifts right beneath the surface. This week has shown that true success isn't about predicting every market twist and turn, but rather about staying flexible and adapting to change as it happens.

See you next Sunday,

Jimit Patel