#17 - WK04

TACO Trade

Welcome to the week that markets learned a new acronym: TACO (Trump Always Chickens Out).

It started Monday when global investors woke up to find President Trump had sent Norway’s prime minister a message demanding “Complete and Total Control of Greenland” because, get this, he didn’t win the 2025 Nobel Peace Prize. Yes, you read that right. Markets didn’t find it amusing. The S&P 500 plunged 2.1% on Tuesday, its worst day since October. European markets crashed alongside it, with Germany’s DAX down 1%, Britain’s FTSE dropping 0.7%, and volatility spiking to levels not seen since November.

Trump had threatened to impose 10% tariffs on eight European countries, including Denmark, France, Germany, and the UK, starting February 1st, escalating to 25% by June, unless Denmark agreed to sell Greenland. European leaders issued strongly-worded statements. NATO allies boosted their Arctic military presence. Trump doubled down, threatening to use “excessive strength and force” to take the “piece of ice.”

Then came Wednesday in Davos. Trump addressed the World Economic Forum, declaring he wouldn’t use military force after all. Hours later, he announced a vague “framework of a future deal” with NATO Secretary General Mark Rutte involving Greenland, calling it “the concept of a deal” in a CNBC interview. Details? Minimal. Something about mineral rights and a Golden Dome missile defense system. Markets didn’t care about specifics, the S&P 500 immediately rallied 1.2%, erasing most of Tuesday’s losses.

The TACO trade was born, or rather, reborn. Investors have now witnessed the pattern: Trump makes extreme threats, markets tank, he backs off with a face-saving “deal,” markets recover. Rinse and repeat.

Meanwhile in Davos, over 60 heads of state gathered under the theme “A Spirit of Dialogue” to discuss global cooperation, AI transformation, and climate action. The irony wasn’t lost on anyone when the week’s biggest story became whether the U.S. president would invade a NATO ally’s territory over a prize he didn’t win.

This week’s newsletter explores a more constructive opportunity emerging from recent geopolitical shifts: Ukraine’s post-war reconstruction and which sectors, particularly construction and infrastructure, stand to benefit most.

Let’s dive in.

Stock Market

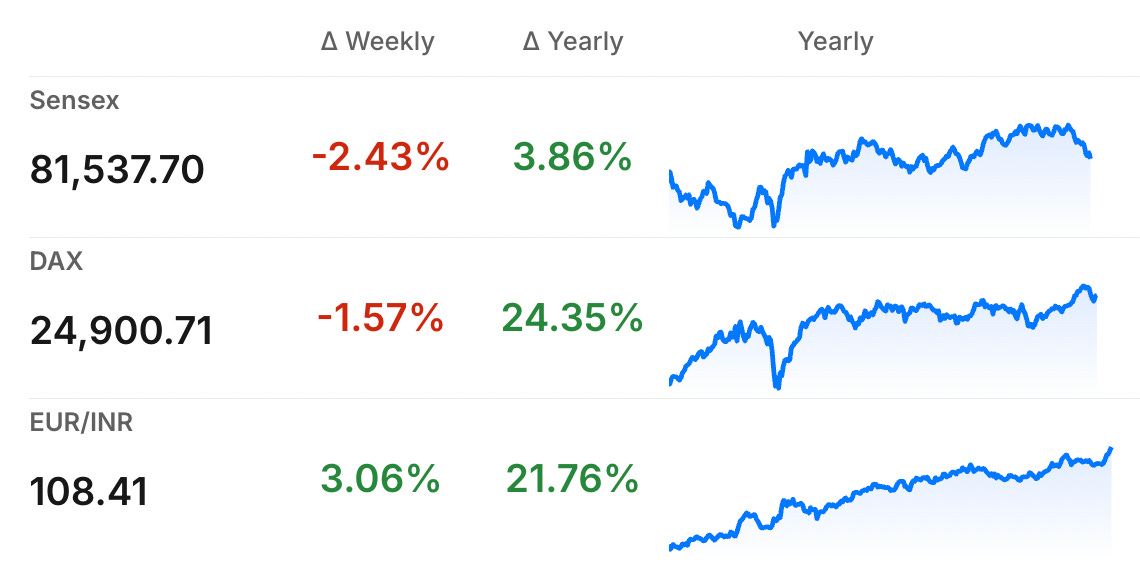

Sensex took a hit this week, tumbling from roughly 83,570 to close at 81,537 on Friday, a drop of nearly 2.4% over the week. Foreign institutional investors (FIIs) pulled money out, and sectors like media and banking saw notable declines, though some recovery attempts were seen in select large caps.

DAX was also under pressure, sliding from around 25,297 last Friday to close near 24,900. While heavyweights like SAP and Siemens Energy performed well, overall sentiment was weighed down by retail and healthcare stocks.

The Euro saw a major jump this week, moving from roughly 105.26 to a high of 108.34 by Friday.

Germany News Roundup

Germany Declines Trump’s Board of Peace Invitation, preferring new, constitutionally acceptable cooperation forms with the US to promote global peace initiatives beyond just the Middle East and Gaza. - DW

Germany Plans to Phase Out DSL by 2035, setting regional cutoffs once 80% have fiber, ensuring fair access, and providing at least one year notice before disconnecting old copper lines. - BR.de

Germany’s Economy Could Grow 1% in 2026, if new U.S. tariffs are avoided, but industrial growth remains fragile requiring reforms to boost competitiveness, reduce bureaucracy, and accelerate permitting processes. - kfgo.com

Germany Reintroduces Electric Vehicle Subsidies, aiming to boost the domestic automotive industry and make environmentally-friendly cars more affordable for families with incomes up to €90,000. - DW

Volkswagen to Open Circular Economy Center, with plans to recycle 15,000 vehicles annually at Zwickau from 2030, investing €90m to reuse parts and reduce reliance on raw materials and carbon footprint. - Euwid Recycling

Germany’s AfD Receives Millions in Public Funding, benefiting from around €500 million in state funds during 2025-2029 despite being monitored for right-wing extremism by intelligence agencies. - DW

Syrian President Delays Planned Germany Visit, citing Syria’s political situation as ceasefire talks progress with Kurdish-led forces, impacting refugee repatriation and reconstruction discussions with German officials. - DW

Germany Includes Chinese Brands in EV Subsidy, with its new €3 billion program promoting electric vehicle adoption among low- to middle-income buyers, boosting affordable Chinese automakers like BYD in Europe. - CnEVPost

India News Roundup

India Avoids Joining Peace Board, raising questions about the initiative's acceptance while India weighs participation amid geopolitical sensitivities and global diplomatic concerns over the new peace body's impact on the UN. - IndiaToday

First Made in India C-295 Aircraft Coming Soon, scheduled to roll out before September, highlighting India-Spain defence collaboration and India's growing manufacturing capabilities in aerospace. - The Hindu

India Signs $3B LNG Deal with UAE, aiming to double trade by 2032 while seeking alternatives amid stalled US negotiations on trade agreements. - CNBC

India-EU Free Trade Deal Near Completion, expected to reduce tariffs and expand market access for key Indian exports amid ongoing sensitive negotiations and regulatory challenges. - Economic Times

American AI Firms Gain from India, Not Charity, profits drive U.S. AI firms offering low-cost AI tools in India to harvest user data and compete against Chinese rivals, not out of charity or goodwill. - India Today

Apple Set to Launch Apple Pay in India, aiming to enable card-based contactless payments first, with future plans to integrate with UPI, intensifying competition in India's digital payments market. - Dynamite News

Opportunity

Russia-Ukraine Peace Deal and Reconstruction - Part 4

Construction and Infrastructure

Ukraine’s reconstruction represents the largest infrastructure undertaking in Europe since World War II, with the World Bank estimating damages exceeding €150 billion.

The Scale of Reconstruction Needs

Ukraine needs to rebuild roads, railways, bridges, schools, hospitals, and residential housing, creating what experts call one of the largest infrastructure projects in modern history. Over 300,000 residential units require reconstruction, alongside thousands of kilometers of roads, hundreds of bridges, and critical public infrastructure from schools to hospitals.

Top German and European Companies to Watch

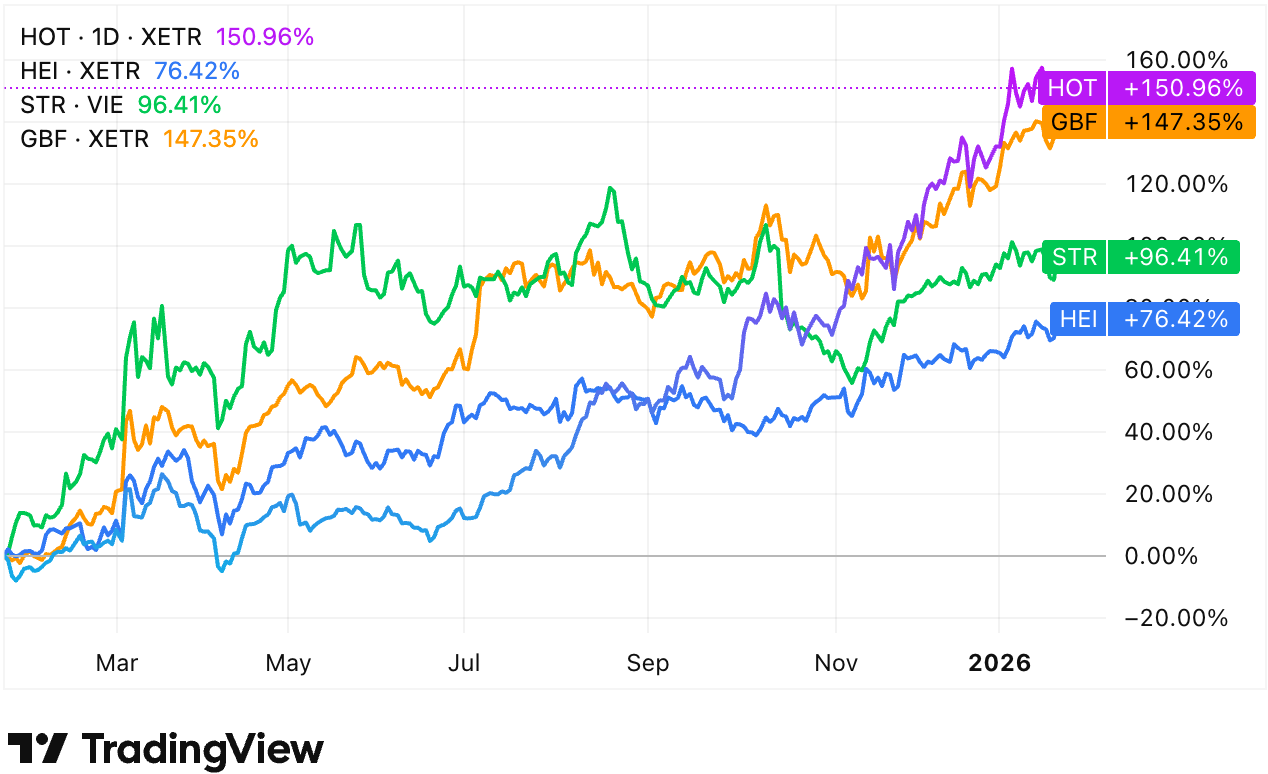

Hochtief AG (HOT) stands out as Germany’s largest construction firm with €33.3 billion in 2024 revenue. The company operates through three divisions, Americas, Asia Pacific, and Europe, with extensive experience in Eastern European mega-projects. Hochtief’s expertise in transportation infrastructure, energy projects, and urban development positions it ideally for Ukraine’s reconstruction contracts. 1

Heidelberg Materials AG (HEI) is the only construction materials company in Germany’s DAX index. The company produces cement, aggregates, and ready-mixed concrete—essential materials for rebuilding roads, bridges, schools, and hospitals. With 3,000 production sites across 60 countries and existing Eastern European operations, Heidelberg can scale quickly to meet Ukrainian demand. 2

Strabag SE (STR) is Europe’s third-largest construction company, generating €17.4 billion in annual revenue. Listed on the Vienna Stock Exchange, Strabag specializes in transportation infrastructure, tunneling, and civil engineering. The company generates 45.9% of revenue from Germany and operates extensively across Central and Eastern Europe, providing established supply chains and regional expertise. 3

Bilfinger SE (GBF) offers engineering services, project management, and industrial maintenance. The company’s expertise in large-scale infrastructure projects and existing Eastern European relationships create opportunities in Ukraine’s systematic reconstruction phase. 4

ETF Options

Lyxor STOXX Europe 600 Construction & Materials UCITS ETF provides diversified exposure to European construction and materials companies, including several positioned for Ukraine reconstruction.

iShares STOXX Europe 600 Construction & Materials UCITS ETF offers similar sector coverage with different weighting methodologies.

Risk Considerations

Security risks remain despite any peace agreement, prioritize companies with diversified geographic revenue streams. Chinese state-owned construction firms will compete aggressively, often with favorable financing from Chinese policy banks. German and European companies must differentiate through quality, EU standards compliance, and political considerations around Euro-Atlantic integration.

Until Next Sunday…

Conclusion

India celebrates its 77th Republic Day on Monday, January 26, with EU leaders Ursula von der Leyen and António Costa as chief guests. The timing is significant, the India-EU FTA, dubbed the “mother of all deals,” is expected to be announced on January 27 during the India-EU Summit.

Once finalized, this agreement would create a market of 2 billion people accounting for almost a quarter of global GDP. For investors, this opens substantial opportunities in sectors from textiles to machinery, particularly as 87% of Indian exports to the EU now face full tariffs after GSP benefits ended January 1.

Next week, we’ll explore how the India-EU trade deal impacts specific sectors and which companies stand to benefit most.

Stay informed, stay invested, and see you next week.

See you next Sunday,

Jimit Patel